Painless Ways In

Let’s skip the boring budget lectures. You already know you should “spend less, save more.” But… why does everyone make it sound so complicated? Most folks try to overhaul their wallets with elaborate spreadsheets or expense tracking apps, then give up the first time they treat themselves to coffee (yep, I’ve been there). Hassle kills momentum. It doesn’t have to be like that.

What if personal finance hacks were simple? Like, “chat-with-your-best-friend-over-coffee” kind of simple. The truth? Tiny wins—automating a bill, splitting your paycheck before you see it, or tricking yourself into saving without even noticing—will stack up faster than you expect. And they work for real people, not just perfect budgeters on TikTok.

I’m not here to judge you for splurging on an extra donut. (Sometimes you need a treat.) Instead, let’s focus on clever ways to save money in everyday life, one imperfect, perfectly do-able step at a time. Ready? Let’s dig in.

Split Your Cash, Ditch The Stress

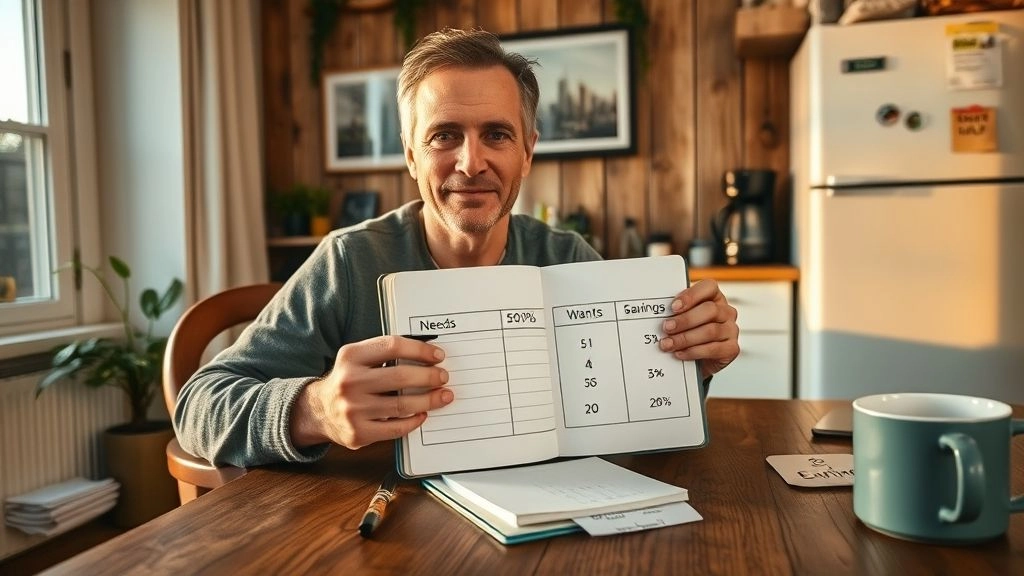

Why Divide Up Your Pay?

Ever deposit your paycheck… and then, poof, it’s gone? Welcome to the club. Here’s a sneakier approach: the bucket method. When you get paid, set up your bank account to automatically slice it into three “buckets”—needs, wants, and savings. You don’t even have to touch a spreadsheet. (Confession: math makes my head hurt before coffee.)

Typical Breakdown Table:

| Category | Percent Of Pay | Example: $2000 Paycheck |

|---|---|---|

| Needs (rent, groceries, basics) | 50% | $1000 |

| Wants (fun, extras, little treats) | 30% | $600 |

| Savings (future you!) | 20% | $400 |

The cool part? It’s flexible. If “20% savings” feels impossible right now, that’s fine. Do 10%, or 5%. Just set something. Think of it as a little act of future kindness. (I started at 5% when I was broke. That five bucks a week felt tiny… for a while. Then I peeked after a few months and was like, “Whoa!”) Set up an auto-transfer; let your bank do the heavy lifting.

For more on making this work on a tighter income, check out these ideas on how to save money fast on a low income. Even skipping one fast food run a week helps if you keep at it.

Bonus tip: Label your buckets. “Vacation” instead of “Savings.” “Treat Yo’self” instead of “Wants.” Makes it more real, and—don’t laugh—it actually helps.

Aim For One Clear Goal

How Do You Pick The Number?

Okay, so that “savings” bucket. What’s it for? Here’s where a lot of people get stuck. If your only goal is “save money” … you’ll lose motivation and tap out fast (trust me, I’ve done it). Instead, pick ONE juicy, specific goal. Like “$5000 for an emergency cushion” or “$300 for that concert next summer.”

Here’s the magic: Break it into smaller wins. You don’t climb a mountain in one leap. You just… take the next step. Divide your big number by the months you want to save. Suddenly, it’s not so scary. (Want to save $1,200 in a year? That’s $100/month. Less than $4 a day. I bet you can do that with a few tweaks.)

Goal-Setting Table:

| Total Needed | # Months | Save Monthly | Save Weekly |

|---|---|---|---|

| $1,000 | 12 | $84 | $21 |

| $500 | 6 | $84 | $21 |

| $5,000 | 24 | $209 | $48 |

Write the goal somewhere visible. I scribble it on a post-it and stick it to my mirror. My buddy Sam draws a goofy “progress bar” with a marker on his fridge. (Yes—grown-ups with stickers still save better.) Celebrate tiny milestones. Maybe with a little dance, or a donut. You do you.

Attack The Big Three First

Are You Overspending Where It Hurts?

You know how everyone tells you to skip the latte? That advice misses the big picture. The fastest way to clever ways to save money? Hit your “big three”: housing, transportation, and taxes. Get creative and you’ll see a difference faster than clipping coupons all year.

Real-Life Comparison:

| Category | Old Way | New Hack | Yearly Savings |

|---|---|---|---|

| Housing | $1200/month (solo) | Rent a room ($700/month) | $6,000 |

| Car | $300/month lease | Bus pass ($80/month) | $2,640 |

| Taxes | Standard refund | File deductions, use tax software | $500+ |

I once moved in with a roommate just for twelve months. Was it awkward sharing a fridge? A little. But I freed up $400 a month… which became a rainy day fund I never would’ve built otherwise. (Also: learning to cook with her weird spices. Blended savings, literally.)

Take a hard look at what you really need vs. want… and attack the big spends with financial hacks to save money. That one bold move can shrink your stress in ways an extra coupon never will.

Set Your Bills On Autopilot

How Can Automation Rescue Your Sanity?

You ever forget a bill, get slapped with a late fee, then swear to do better? Same. The fix? “Set it and forget it.” Most banks let you automate bill payments and automate your transfers to savings accounts after payday. When the money leaves before you can even miss it, there’s no room for slip-ups or guilt (…or my classic “oops, I forgot rent again” panic).

One of my best money hacks: Ditching physical mail and wrangling all my bills online. Now, I don’t miss payments. No random fees. No drama.

If impulse spending is your weakness, try the cash/debit card-only method for your “play” money. When the cash is gone, you’re done until next pay. (Kind of old-school, but hey, old-school works for a reason.)

Sneaky Savings Through DIY

Is Your Latte Habit Bleeding You Dry?

We all have our “little treats.” For me, it was fancy lattes… $5 a pop, sneaking into my budget more than I’d ever admit to a financial advisor. Then I read a thread recommending making coffee at home—yeah, I rolled my eyes. But I committed to brewing my own for a single month. Guess what? I saved over $80, and… my house started smelling amazing. (Small perks, big payoff.) Redditors have even calculated their own “hidden” expenses and shared hacks like this on their favorite boards—turns out you can learn a lot from strangers complaining about their bills!

Coffee Savings Table:

| Habit | Yearly Cost (buying out) | Yearly Cost (DIY) | Yearly Savings |

|---|---|---|---|

| Daily Latte | $5 x 300 = $1,500 | $0.25 x 300 = $75 | $1,425 |

Try a similar approach elsewhere. Bulk cooking your meals, hitting thrift stores, using cashback apps—these are the top 10 brilliant money-saving tips for everyday life. If it sounds boring, just track your “saved by DIY” number for one week, and see if the game starts to feel real.

Emergency Funds That Don’t Hurt

How Much Do You Really Need?

Let’s be real—saving six months’ expenses is a tall order. If that number makes you feel faint, start with $500. That’s enough to buffer a car breakdown, surprise vet bill, or losing your phone (been here… still salty). Every dollar in your “oh crap” fund buys serious peace of mind.

I started by funneling $10 a week into a separate account. Out of sight, out of mind. The first time I actually needed it (flat tire, thanks universe!), I felt like a genius. Suddenly you’re not living on edge. It snowballs from there.

Impulse Control: The “Wants” List

How Do You Outsmart Your Inner Shopper?

All those “must-have” gadgets? Write them down in your phone’s notes app. Give it thirty days. Most will magically vanish from your “urgent” list—promise. (I still want a new tablet… but after a month, the urge faded.)

This trick saved me over $500 in impulse purchases last year. That’s a vacation I probably wouldn’t have taken otherwise.

If you’re still itching to buy, try only using cash/debit for fun stuff. When the envelope is empty, you’re done. Turns your “YOLO!” swipe into “eh, maybe next month.” This method—straight from pro budgeting hacks—really is free money hacks in disguise.

The Debt Destroyer Mindset

Should You Fear Your Credit Cards?

Ah, credit cards. Love ’em or hate ’em, they trip up even the savviest savers. Here’s my personal finance hack: Tackle your highest-interest balances first (the snowball or avalanche method… pick whichever name makes you feel cooler). And please, delete saved card info from your favorite shopping sites. It’s like putting cookies on the top shelf—annoying to reach, but effective.

If you’re overwhelmed, know you’re not alone. Sometimes it’s worth reaching out to a financial counselor—no shame in it! They can help design a payoff plan that actually works. Celebrate every debt destroyed. Even paying off a $100 balance feels like winning a gold medal. Financial hacks to save money often start with “attack the high-interest monsters first.”

Track Wins, Not Pennies

Why Celebrate The Small Stuff?

Last tip? Stop obsessing over every nickel. Try this: For every no-spend day, give yourself a gold star (or a silly sticker, if you’re me). Focus on your progress, not perfection. Take inspiration from books like “Rich Dad Poor Dad,” or just journal your own wins. You’ll see your mindset shift over time.

Share your journey with a friend—or even shoot me a message if you want! The point is: celebrating tiny victories makes this money stuff feel lighter, more fun, and a little less lonely.

Wrapping Up—You’ve Got This

So, what did we cover? We dodged boring spreadsheets, split our cash into sanity-saving buckets, and found ways to trick ourselves into saving, almost without noticing. We attacked the big expenses (forget lattes, go after that rent!), tried some how to save money fast on a low income ideas, and set realistic goals without the stress. Plus: we automated bills, built that itty-bitty (but mighty!) emergency fund and even turned impulse shopping into a game.

Personal finance hacks aren’t about perfection. They’re messy, human, and seriously satisfying once you start stacking a few wins. The weird thing? This stuff gets easier. And more fun. Soon, you’ll see your progress—and you might even help a friend along the way. (That’s a real glow-up, trust me.)

So—what’s your first step? Maybe it’s an auto-transfer, or writing your goal on your bathroom mirror, or just sticking to coffee at home for seven days. Don’t overthink it. Just try one. Let’s build those money-saving muscles… real people, real results, no perfection required. If you want more inspiration, here’s a good place to start exploring the top 10 brilliant money-saving tips.

Cheering you on, always. And if you found even one tip helpful, go ahead—reward yourself with that donut. You’ve earned it.