However, there are strategies that can make a private K–12 education attainable.

The typical private school tuition in 2021 for K–12 was $11,200 annually, according to Private School Review. Elementary school averaged $10,100 and high school about $15,000. In some major metropolitan areas like New York and parts of California, tuition can exceed $30,000 per year.

Still, many families with children in private schools don’t actually pay those full rates.

About 28% of private school students receive some kind of financial assistance, according to Education Data, and those awarded grants receive an average of $11,500. Another 5% of students get tuition reductions averaging $10,000 because their parents are employed by the school.

We consulted financial aid specialists and other advisers about the various ways to score discounts (or at least lower your tax burden) to make private schooling more financially feasible.

How to Cover Private School Costs (Without Financial Ruin)

529 Savings Plan

Good news: Federal rules for 529 plans were recently updated so they can be applied to K–12 education, not solely college. You may use up to $10,000 per year from a 529 account for K–12 expenses. Before doing so, verify your state’s rules.

“Some states have not yet aligned with the new federal guidance,” Bambridge notes. Remember, you aren’t required to have your 529 in the state where you live, so if your state doesn’t permit it, consider opening a plan in another state that does.

A 529 Savings Plan lets you invest tax-advantaged funds as long as withdrawals are for qualified expenses. It’s akin to a 401(k) or IRA but specifically geared for education, Bambridge explains.

You can open a 529 for your child online without an annual fee or a large initial deposit, says Olivia Summerhill, a CFP and divorce financial planner in Seattle. “From my experience, older relatives often are unsure how to gift money properly for grandchildren’s education,” Summerhill says. “It’s fairly straightforward, and anyone can contribute to another person’s 529.”

In short, the account owner isn’t the only one who can add money to the 529.

Coverdell Education Savings Account

This is a trust or custodial account allowing contributions up to $2,000 a year, which can grow tax-free, says Alistair Bambridge, a New York partner with Bambridge Accountants.

Funds must be used for qualified expenses like tuition, fees, books and supplies. While contributions aren’t tax deductible, the money grows tax-free until it’s withdrawn, Bambridge says. One limitation: If your adjusted gross income exceeds $110,000 (or $220,000 if filing jointly), you’re ineligible to contribute to a Coverdell ESA.

Overall, Coverdells have become less popular because 529 plans offer more flexibility.

State-by-State Discounts

Certain states provide their own private school assistance programs, Bambridge says. For instance, in Alabama, parents with children in schools deemed “failing” can apply to move to a non-failing school and receive a $2,814 offset. In Louisiana, families can receive up to $5,000 per dependent for K–12 Louisiana-based private schools.

Check here to find options in your state.

Roth IRA

A Roth IRA is an individual retirement account that permits qualified withdrawals tax-free for eligible educational costs. “Although primarily for retirement, the Roth IRA’s flexibility allows you to withdraw contributions tax-free provided the account has been open at least five years,” Bambridge says.

In 2021, annual contributions were capped at $6,000 (or $7,000 if you’re 50 or older). So investing $5,000 a year for 15 years could yield $75,000 in tax-free contributions withdrawn.

Financial Aid

Apply to the school’s aid program even if you think your income is too high, advises Eric Kim, program director at LA Tutors. Many schools allocate financial aid on a sliding scale. So even households earning more than $200,000 may qualify, depending on factors like how many children attend the school, how many are in college, and regional considerations. Admissions decisions usually come first, then aid offers are made based on multiple elements, including the school’s aid budget.

Most private schools use the National Association of Independent Schools Parents Financial Statement to evaluate need. Typically, you only need to complete this form once to apply for financial aid across multiple private schools. Be prepared to reveal your full financial picture, including wages, debts, assets (cars, bank balances) and other expenditures.

Forms don’t always capture the whole story, so experts suggest appending a letter that outlines circumstances not obvious on paperwork. Do you support additional family members? Are there extraordinary expenses? This is your chance to explain.

The critical step is submitting all documents on time or early (many deadlines fall on April 15), though some institutions have earlier cutoffs.

Need and Desire

Financial aid from private schools hinges on need — and also on how much the school wants to enroll that particular student and family, says Alina Adams, a New York school adviser and author of “Getting into NYC Kindergarten.”

“I’ve seen families submit identical financial information to five different schools and receive five wildly different scholarship packages, ranging from nothing to modest discounts, to half off, to 75% off, and occasionally a full scholarship,” Adams says. “Same child, same parents, same income, very different outcomes.”

It often depends on what gaps the school is trying to fill. That might include racial, ethnic or religious diversity, or a particular profession in a parent. Or perhaps your child is the type of student the school believes will enhance their reputation. Maybe your child excels in an extracurricular pursuit that could reflect positively on the institution. “They may not be termed ‘merit scholarships,’ but need-based awards frequently boil down to your child’s unique profile,” Adams says.

Although much of this is beyond your control, you can improve your odds by explaining to the school how your child would be an asset. Is he an outstanding trumpet player? A natural speller likely to compete in bees?

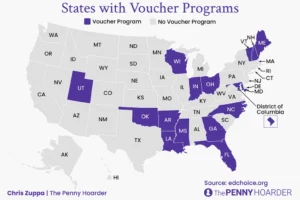

State Voucher

Many states offer private school vouchers, sometimes called school choice or scholarship programs. These initiatives allocate public education funds for families to apply toward private school tuition.

Each state has its own eligibility rules. In some states, households must fall within a certain percentage of federal poverty guidelines. Other states require students to pass a test to receive a voucher. To check whether your state has a voucher program, click here.

Danielle Braff is a contributor to Savinly.