Over roughly two and a half years, self-described “bad saver” Matt Wiley quietly accumulated $4,300 without consciously trying to save.

“It feels odd to say ‘I saved,’ since I didn’t really do anything,” he admitted.

Even though he worked as an editor at Savinly at the time, Wiley confessed he’d never been adept at putting money aside.

“I don’t have a great explanation for why it’s been hard — I’ve just never been good at forcing myself to set money aside and leave it alone.”

In early 2015, Wiley learned about a savings app called Oportun (previously Digit) from a friend of his wife who was already using it to build up savings. Since launching as an automated savings tool that turned Wiley into a genuine saver, Oportun has broadened its offerings well beyond simple savings.

So how did Oportun help this reluctant saver tuck away more than $4,000? And could it work the same way for you?

In this Oportun app review, we’ll walk through the app’s features so you can see how it helps people save and manage money in one place — with, let’s be real, minimal effort.

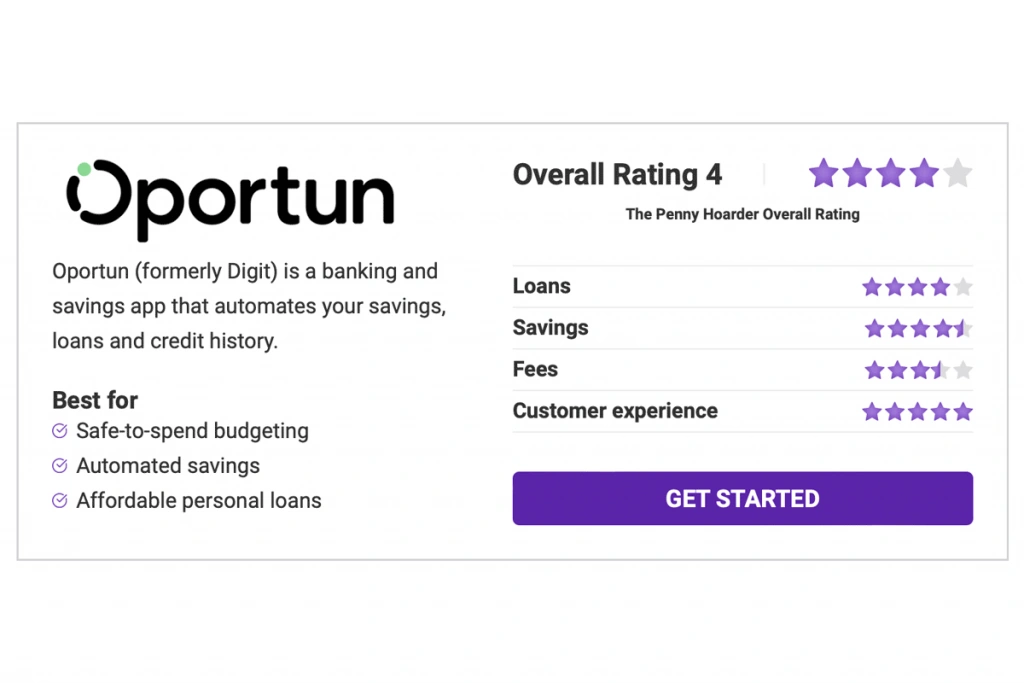

Oportun App Review: Account Options

For this 2024 review, we examined the app’s full range of services, including savings accounts, credit cards and personal loan products.

When you create an Oportun account, you can opt to use just the savings tool, open an Oportun credit card, or apply for a personal loan.

Oportun Credit Card

- Credit limits up to $1,000

- Accepted wherever Visa is accepted

- No established credit history required to apply

This card carries APRs from 24.90% to 29.90%, and credit lines typically range from $330 to $1,000. As a Visa card, it’s widely usable at most merchants.

How Oportun Determines Your Savings

To help ensure you only save what fits your budget, you can create as many—or as few—savings goals as you like. When you set up a goal, Oportun will estimate the daily amount it plans to transfer to hit your goal by the date you choose.

You fund Oportun savings with a linked checking account; cash deposits aren’t supported.

Oportun offers a free 30-day trial, after which the service costs $5 per month.

Oportun Set & Save™

- AI-informed savings tailored to your finances

- Open-ended or target-based saving options

- No withdrawal limits or minimum balance requirements

Automatic saving is Oportun’s specialty. The app began as an auto-saving tool before adding personal loans to the platform.

Unlike many savings apps, Oportun doesn’t force you to pick a final target for every goal. You can add a goal amount and an end date if you want, or leave them open-ended, much like Wiley did, saving whatever you can.

When you connect your bank account, low-balance protection is enabled by default so Oportun doesn’t transfer more than you’re comfortable with. The default threshold is $25, but you can customize it.

What Sets Oportun Apart

What makes Oportun unique is that it doesn’t depend on you to stick to a rigid savings schedule that may not suit your life. Instead, it analyzes your income and spending behavior and adjusts how much it saves for you each day.

“I liked the idea of an algorithm taking small amounts out in ways I wouldn’t notice,” Wiley said. “I was on my first job after college and living paycheck to paycheck, so I hadn’t been saving at all. It seemed worth a shot.”

Oportun Personal Loans

- APRs up to 35.99%

- Encrypted and secure application process

- Vehicle title can be used as collateral for larger loans

One advantage of an Oportun personal loan is that it can be used to consolidate existing debt. Taking on significant personal debt can be risky — we suggest exploring savings and budgeting strategies before taking out a new loan.

Still, Oportun emphasizes reasonable loan rates, educational resources about borrowing, and helping borrowers build credit by making on-time payments.

Digit’s Evolution into Oportun

Oportun began as Digit, a savings app, and expanded to include loans and credit cards after being acquired by Oportun in December 2021.

It doesn’t currently provide other banking products like checking accounts or debit cards, though those could be added down the line.

Oportun Fees

Unlike some rivals, Oportun charges a flat $5 monthly subscription for its service. The first 30 days are complimentary.

For Wiley, the fee was a small price to pay for the $4,300 he amassed essentially without thinking and the peace of mind of not worrying about his bank balance.

“Way less than Netflix,” he said.

Oportun doesn’t charge standard bank-style fees such as overdraft or minimum balance charges.

When personal loans are approved, Oportun applies an Administrative Fee equal to 8% of the original loan amount.

Oportun Customer Experience

When you connect your bank account, it’s crucial that the linked app is user-friendly and reliable. Oportun delivers on both fronts.

The app has ratings of 4.7 out of 5 in the App Store and 4.5 out of 5 on Google Play, with hundreds of thousands of reviews backing those scores.

As with any app tied to your bank, Oportun doesn’t have physical branches where you can speak with someone in person. However, its online support is available. An online help center addresses common questions, and you can email customer support for account-specific issues and get a timely reply.

Concerned about handing your finances to AI? Don’t be. The app lets you establish limits for where and when it can move funds — and in practice, allowing it to operate often works well.

“I’m definitely into passive saving,” he said. “For folks like me [the so-called ‘Bad Savers’], not having to think about it is the best way to build savings.”

Is Oportun a Good Fit for You?

Oportun suits people who want a financial tool that removes the mental load of money management.

If you’ve struggled to consistently save, pay bills on time, build retirement savings, or succeed with a conventional budget, this automated solution could be a good match.

Oportun doesn’t support joint accounts, so it’s not ideal if you need a shared account. It also doesn’t accept cash deposits, so it’s less suitable if you’re primarily paid in cash.

Pros and Cons of Oportun

Below are the primary advantages and downsides of using Oportun for savings, loans, credit cards and overall money management.

- Automated savings based on what you can realistically afford

- Personal loans with relatively high approval rates

- Visa credit card option with limits up to $1,000

- Flexible ways to set and manage savings goals

- Low-balance protection without extra fees while saving toward goals

- 30-day free trial

- No free tier — costs $5 monthly

- No option to deposit cash

- No joint account capability

- No longer offers investing

- No longer provides full banking services

Frequently Asked Questions (FAQs) About Oportun

Here are answers to common questions to help you decide whether Oportun is the right place to manage your savings.

Oportun is a deposit product provided through Pathward that you can use for savings, personal loans and credit cards. You control everything from the Oportun app, though on the backend your money is allocated across accounts for loans, credit card payments and savings. Oportun itself is a fintech company, not a traditional bank.

Yes — Oportun began as Digit, a San Francisco-based startup founded in 2013 by business and finance expert Ethan Bloch. It raised more than $60 million from venture firms before being bought by Oportun in late 2021.

Only you can determine whether $5 per month is worth it. In exchange for that fee, the app offers convenience and assurance: automated savings growth, help keeping loan payments on schedule and potential credit-building. If you don’t need that automation, several online savings options have no monthly charge.

The chief benefit of Oportun is automation: it uses smart technology many budgeting tools don’t to set aside money safely. For many users, the main drawback is the monthly fee, though other budgeting apps also charge.

Definitely not! The savings feature allows you to transfer your balance from Oportun back to your linked bank account at any time. An Oportun account functions like a virtual savings container in your name that you can access and control. Your funds held in Oportun are secure.

Riley Foster is a Certified Educator in Personal Finance® and founder ofHealthy Rich, a resource for inclusive, budget-free financial education. Riley has written about work and money for outlets including Forbes, The New York Times, CNBC, NextAdvisor, Insider and Inc. Magazine. Former Savinly staff writer Jordan Meyers contributed reporting to this article.