Why Is Money Always So… Slippery?

Okay, pause. Tell me if this sounds familiar: You get paid, you feel rich, you treat yourself. A new hoodie? Why not. Extra-large latte? Toss it in. Then—bam—three weeks later, your account balance is lower than your motivation at 7am on a Monday.

Isn’t it wild how spending can feel totally normal, almost invisible, until it isn’t? Like, I used to joke with friends that my bank balance was playing hide-and-seek… and let me tell you, it’s a champion hider.

This is why I’m slightly obsessed with budgeting “rules.” Not because I dream of spreadsheets (seriously, I don’t), but because I finally found one that doesn’t feel like punishment. If you’ve ever asked “what is the 70-10-10-10 rule for money?” then sit tight—it’s about to make your whole money deal waaay less stressful.

Splitting Your Money Pie: Wait, Four Ways?

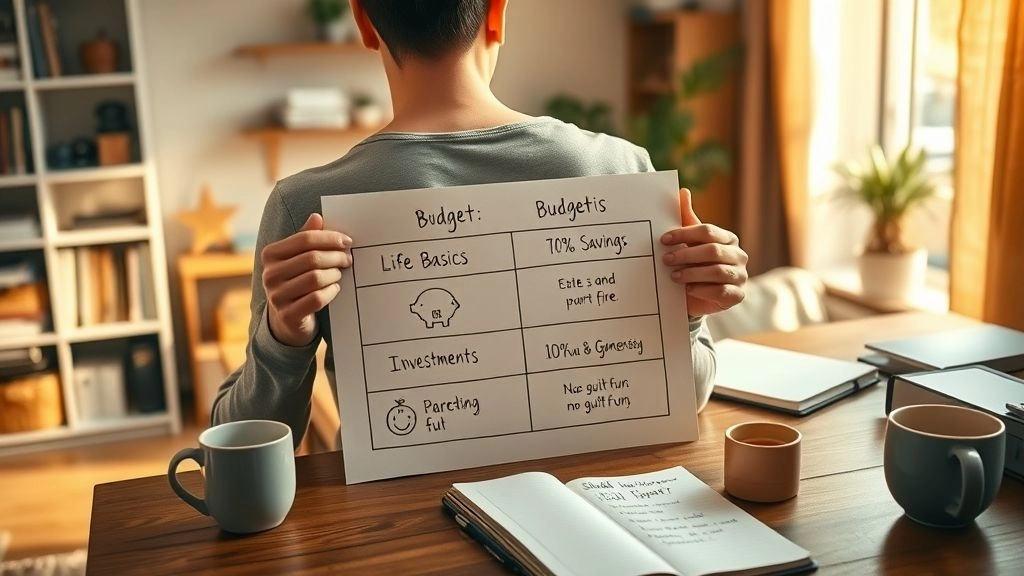

What Exactly Is the 70-10-10-10 Rule?

Let’s break it down, friend-to-friend. The 70-10-10-10 rule is… well, just that: Split your take-home money into four “buckets” every month:

- 70% – Life basics (rent, food, bills, stuff you honestly can’t skip)

- 10% – Savings (building your cushion, for when life throws shade)

- 10% – Investments (this is for Future You—think retirement or little investing apps, not stock market gambling)

- 10% – Fun & generosity (treats, helping out a friend, a donation—no guilt zone!)

Simple, right? No complicated math, no fancy finance degree. You just… divvy up what you’ve got coming in, and poof—the stress melts a bit.

I first stumbled on this method after a seriously embarrassing overdraft moment in college. (Picture: me, declining card, red-faced, behind a grandma buying three avocados.) Ever since then, I’ve clung to this method like my last coffee at finals.

How Is This Different From Other Budgeting Rules?

Maybe you’ve seen those 50/30/20 rules. Those are fine! But honestly, what if you live somewhere expensive, or you’re just starting out and some months you basically are a can of beans? The 70-10-10-10 method feels more forgiving. Because real life… isn’t one-size-fits-all.

| Budgeting Rule | Needs | Wants | Savings/Investments | Extra (Giving/Fun) |

|---|---|---|---|---|

| 50/30/20 | 50% | 30% | 20% | N/A |

| 70-10-10-10 | 70% | 10% | 10% (Savings) + 10% (Investments) | 10% |

See—for students or anyone with an unpredictable budget, the extra categories are like a buffer. (For relatable, real-life takes, I love this University budget example for students—it literally shows you how to break things up!)

The Buckets in Real Life

That 70%: Where Does It Go Anyway?

This is the big slice of the pie. It’s boring, but it keeps the lights on—so, rent, groceries, bus pass, phone bill. Sometimes “essentials” sneak up on you, like when your old laptop wheezes its final wheeze before an exam. Been there. (Pro tip: put aside a small “oops fund” inside this category for those “please not today” moments.)

Ever notice how “essentials” can start to quietly expand? Like, your streaming subscriptions, or the expensive sandwich place by campus. If you want a quick way to spot the budget-draining stuff, literally write down every purchase for a week. It’s awkward at first… but it’s like turning the kitchen light on and seeing where the ants are coming from. Suddenly, you realize—wow, that’s $40 a month on soda? Ouch.

By the way, for a no-stress example, the University budget example for students breaks this down so even non-math folks can follow along.

Savings: The “No More Panic!” Bucket

You know how in movies, people smash open their piggy banks? Savings is basically that… but without the dramatic slow-mo. The 10% for savings isn’t just about emergencies (like car trouble or lost wireless headphones). It’s peace of mind.

Confession: When I started putting away even like $20 a month, I got addicted to the feeling… less heartburn if my tire’s flat. Honestly, it’s the grown-up way to buy yourself just a little calm.

And you don’t have to start big—just start. Set it to auto-transfer, and forget about it. If you’re a student, check out this step-by-step How to make a budget plan as a student? guide—real humans wrote it, so it’s not dry at all.

Investing: Don’t Be Scared, Future You Will Thank You

Look, “investing” sounds intimidating. Like you need a monocle and a top-hat. But the 10% here is all about little steps. Retirement accounts? Maybe. An app that lets you buy $5 worth of index funds? Perfect.

I started with one of those “round up your purchase” apps, which is just, like… every time you buy a bagel it puts the spare change into investments. I didn’t notice it was happening. Three months later… hey, free lunch money out of nowhere!

You can go fancy if you want, but consistency is the magic. Just like the Monthly Budget plan example for students says, it’s less important where you invest at first—just that you do it. Baby steps.

| Investment Type | Risk Level | Potential Return (Avg.) |

|---|---|---|

| Savings Account | Low | 2-4% |

| Index Funds | Medium | 7-10% |

| Stocks | High | Varies (can be 10%+) |

Fun & Generosity: Don’t Skip This One!

Here’s the thing… budgeting gets a bad rap because it sounds strict. But the last 10%? It’s literally for joy. That could mean going for pizza with your friends after finals, or surprising someone with coffee, or even giving to a cause you care about.

I put “generosity” as the label, but honestly, sometimes self-kindness is generous too! I used my last fun-money on a plant for my desk. Did it help my productivity? Nope. Did it make me smile every day? Yep. Totally worth it.

Still figuring out what “fun” means for you? Try this Simple budget plan example for students free setup. There’s no wrong way to do this.

How To Make It Actually Work (and Not Give Up After a Week)

First Step: Track Just One Paycheck

No one sticks to a plan if it feels impossible. So, pick your next paycheck—just one!—and challenge yourself to split it the “70-10-10-10” way. Don’t overthink it. Even if the percentages are rough, you’ll get a sense for where your money is sneaking off to.

And if you already have a side hustle, scholarship, or a part-time gig (hello, delivery bike warriors!), combine your income. The method doesn’t care if it’s from waiting tables or tutoring calculus.

For a detailed walkthrough, try the How do you create a simple budget plan? worksheet and actually print it out. Yeah, with real paper. It’s surprisingly satisfying.

Biggest Challenge: All the “But What About…” Questions

Real talk—life gets messy. Car breaks down, textbook prices skyrocket, your roommate forgets to pay their half of the internet bill. That’s normal. Revisit your buckets, and shuffle if you need to. It’s flexible; you’re not a robot.

If you’re wondering “how do you create a simple budget plan?” when your income jumps around (looking at my fellow freelancers!), focus on percentages, not amounts. Some months are feast, some months are noodles—but if you keep the ratios, you’re already ahead.

Good news: even with a tiny budget, this approach works. As you earn more, the habits stay, just on a bigger scale. Like financial muscle memory.

Got Roommates, or Shared Expenses? You’re Not Alone

Trying to budget when other people are involved (roommates, partners, family)? Tricky, but not impossible. Start with what you can control—your portion, your spending. Then, have “the talk.” Not the big, dramatic one, just… “Hey, wanna try this split-the-buckets thing for groceries?”

It takes guts to be the money-nerd friend at first, but someone has to do it. You might be surprised who secretly wants to try a Monthly Budget plan example for students.

Why the 70-10-10-10 Rule Works (and Why I’m Still Using It)

If you’ve read this far (bless you, patient soul), I hope you’re picking up on the real magic of the 70-10-10-10 rule: it’s not about micromanaging every penny. It’s about giving yourself a blueprint, so you don’t have to do the “wallet panic” dance every payday.

I won’t pretend I’m perfect—last month I went waaaay over in the fun bucket for festival tickets. Dipped a bit into savings, too. But… I could see it, it was intentional, and I adjusted next month.

If you want reassurance before jumping in, chat with someone who has tried any “simple budget plan example for students free” (even if you’re not technically a student). The internet is bursting with stories—some hilarious, some cautionary—but nearly all say the same thing: having a plan is better than winging it.

And bonus: You realize you can say yes sometimes. To the impromptu road trip, or the new basketball shoes, or the fundraiser your bestie roped you into. No guilt. That’s worth something, right?

Trying It Yourself: Final Thoughts

Let’s be real: money will always be a little slippery. But if you’re tired of going through life in “Where Did It All Go?” mode, the 70-10-10-10 rule is your gentle nudge toward sanity. You don’t need a finance degree, you don’t need a fancy app—heck, you just need four jars and some labels (or four folders in your phone banking app!).

Start small. Split your next paycheck. Celebrate small wins (like not panicking when you see your balance). Poke around the How to make a budget plan as a student? guide, even if it’s been years since you graduated. Ask your roommate, “Wanna try a crazy budgeting challenge?” Worst case, you’ll get a good story.

So… what bucket will you start with? Essentials, fun, charity, or finally saving up for that emergency pizza fund? Shoot me a message or drop a comment. I’d honestly love to know. Because if there’s one thing I’ve learned, it’s that talking about money—messy, human, real money—makes it a whole lot less scary.