Experts often recommend introducing children to money concepts early on.

Still, parenting styles differ widely, so there isn’t a universal rule for exactly what a child should learn about finances at each age.

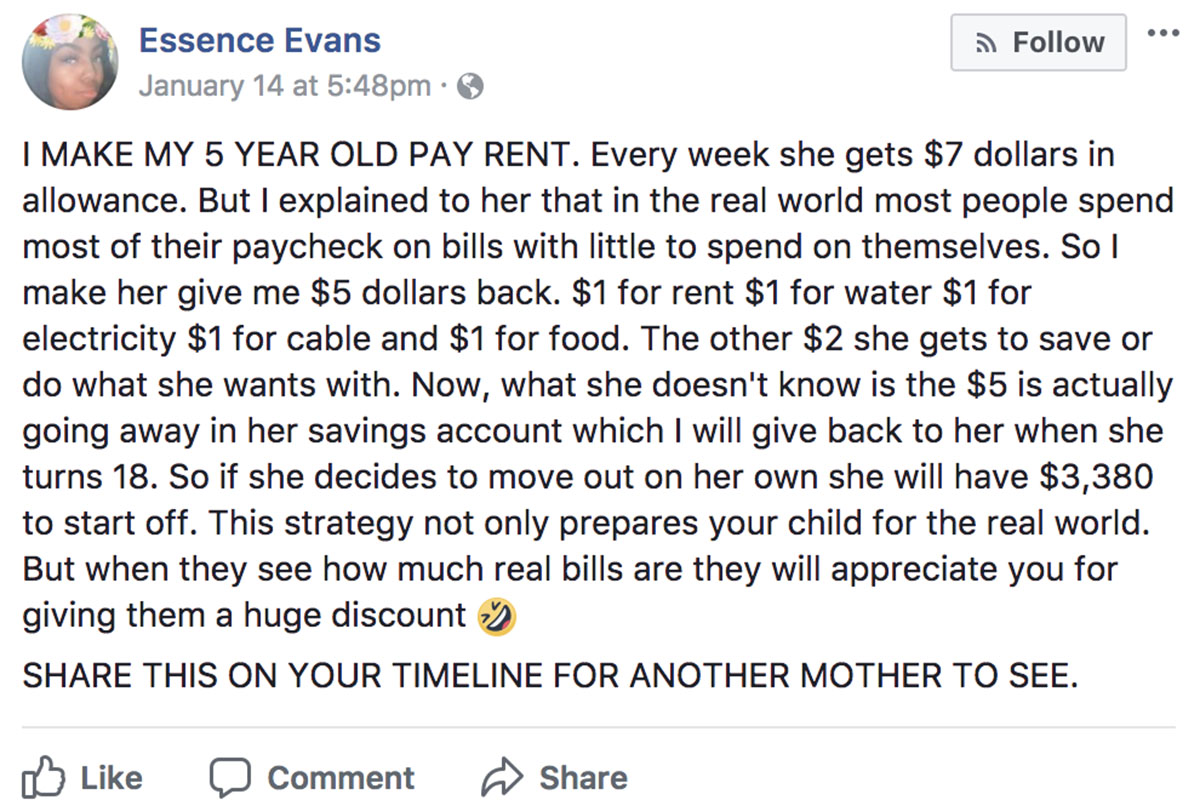

On Sunday, Essence Evans took to Facebook to explain howshe has her 5-year-old daughter “pay rent.”

Yes — the child “pays rent,” along with contributions for utilities and groceries.

But before you react, hear the whole thing. It’s not as harsh as it sounds.

Evans describes in her post that from the $7 weekly allowance she gives her daughter, she requires $5 to be returned — a dollar each for rent, water, electricity, cable and food.

That leaves the child with $2 per week to either save or spend as she pleases. Evans says she uses this method to teach her daughter that “most people spend most of their paycheck on bills.”

Evans uses the allowance rule as a learning exercise. She isn’t literally collecting funds from her toddler to cover housing or meals (after all, that small sum wouldn’t meaningfully contribute).

She added that, without her child’s knowledge, she’s tucking that money into an account the girl will be able to access at 18.

I personally think it’s a reasonable way to introduce a youngster to budgeting and prioritizing money for essentials. Often, kids don’t encounter the realities of paying bills until they’re adults with actual obligations and the consequences that follow if they haven’t learned to budget.

Additionally, I agree with the perspective that allowance can be considered a privilege rather than an entitlement. This mom could have simply handed her daughter $2 each week (or nothing at all) and separately placed $5 a week into savings — but that would have missed out on the practical money-management lesson.

Not everyone who saw Evans’ post felt the same way. Since Sunday, the post has attracted more than 42,000 comments, over 307,000 shares and in excess of 219,000 likes and reactions. It’s been covered by outlets including Scary Mommy, Working Mother and Romper.

Many responses criticized Evans’ technique for teaching finances, with commenters saying “let kids be kids.” Some argued that age 5 is far too young to be introduced to household expenses, while others suggested it could cause undue stress or anxiety.

Others warned the weekly practice could instill a mindset of perpetual bill servitude, and some readers quibbled that other real-life costs weren’t included in the breakdown.

At Savinly, we’ve covered other unconventional methods parents use to teach their children about money.

One father drafted formal contracts for his two daughters, outlining specific tasks required to earn their allowance, complete with yearly renegotiations.

Another parent sent his teenager away for a month with no phone, no contacts, no stable place to stay and very limited funds — a hard lesson intended to teach independence and the value of work.

Even celebrity chef Gordon Ramsay has said he won’t leave his fortune to his four children to avoid spoiling them.

Every family will differ in how they choose to teach essential life skills. My hope is that financial literacy is one of those lessons parents make sure to pass on — however they elect to do it.

Nicole Dale is a staff writer at Savinly. She focuses on parenting and personal finance topics.